The optimal portfolio concept falls under the portfolio theory.

The theory assumes that investors fanatically try to minimize risk while striving for the highest return possible.

The theory states that investors will act rationally, always making decisions aimed at maximizing their return for their acceptable level of risk.

The optimal portfolio was used in 1952 by Harry Markowitz, and it shows us that it is possible for different portfolios to have varying levels of risk and return.

Each investor must decide how much risk they can handle and then allocate or diversify their portfolio according to this decision.

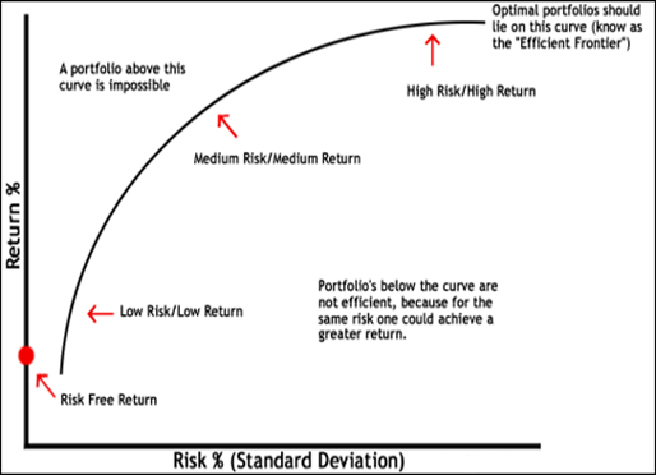

The chart below illustrates how the optimal portfolio works.

The optimal-risk portfolio is usually determined to be somewhere in the middle of the curve because as you go higher up the curve, you take on proportionately more risk for a lower incremental return.

On the other end, low risk/low return portfolios are pointless because you can achieve a similar return by investing in risk-free assets, like government securities.

You can choose how much volatility you are willing to bear in your portfolio by picking any other point that falls on the efficient frontier.

This will give you the maximum return for the amount of risk you wish to accept.

Optimizing your portfolio is not something you can calculate in your head.

There are computer programs that are dedicated to determining optimal portfolios by estimating hundreds (and sometimes thousands) of different expected returns for each given amount of risk.

{kind=link}